The Warm Homes Plan: What Developers Need to Know Beyond the Future Homes Standard

On 21 January 2026, the UK government published the Warm Homes Plan — a £15 billion programme to upgrade Britain's homes, cut energy bills, and accelerate the shift away from fossil fuel heating. It has been described as the largest home upgrade investment in UK history.

For most of the industry commentary, the focus has been on retrofit — insulating existing homes, replacing gas boilers with heat pumps, and supporting fuel-poor households. That makes sense. The vast majority of the UK's housing stock was built before the 1980s, and much of it is over a century old. Retrofit is where the scale of the challenge lies.

But for housebuilders and developers, the Warm Homes Plan contains critical signals about the direction of new-build policy that go well beyond what the Future Homes Standard alone tells you. And for SME developers in particular, understanding the relationship between the two — and the practical implications for design, procurement, and sales — is essential for protecting viability and programme

The Warm Homes Plan and the Future Homes Standard: How They Connect

The Future Homes Standard (FHS) sets the technical requirements for new homes — the 75% carbon reduction target, the expectation of heat pumps as the default heating system, mandatory solar PV, enhanced ventilation through Mechanical Ventilation with Heat Recovery (MVHR), and overheating mitigation through dynamic thermal modelling. We covered this in detail in our previous article on Parts L, F, O, and S.

The Warm Homes Plan sits above the FHS as a broader policy framework. It confirms the government's commitment to implementing the Future Homes Standard and provides the wider context — funding mechanisms, supply chain targets, consumer incentives, and market signals — that will shape how the FHS is delivered in practice.

Think of it this way: the Future Homes Standard tells you what your homes must achieve technically. The Warm Homes Plan tells you why the government is committed to it, how it intends to support delivery, and where the market is heading.

For developers, understanding both is essential. The FHS gives you specifications. The Warm Homes Plan gives you market intelligence and commercial context.

What the Warm Homes Plan Confirms for New-Build

Solar PV and Clean Heating Are Now Standard — Not Optional

The Warm Homes Plan explicitly states that new-build homes from 2026 will require solar panels and clean heating as standard under the Future Homes Standard. The government's ambition is to triple the amount of solar on domestic rooftops by 2030.

For developers, this removes any remaining ambiguity. Solar PV is a baseline requirement, not an optional upgrade or a marketing feature. The practical implications are significant: roof design must accommodate panels from the outset, with orientation and pitch optimised for generation rather than treated as an afterthought. Electrical infrastructure must be sized for solar generation, battery storage, and EV charging simultaneously. And the interaction between these systems must be considered as an integrated energy package from RIBA Stage 2, not as separate technologies bolted on during detailed design.

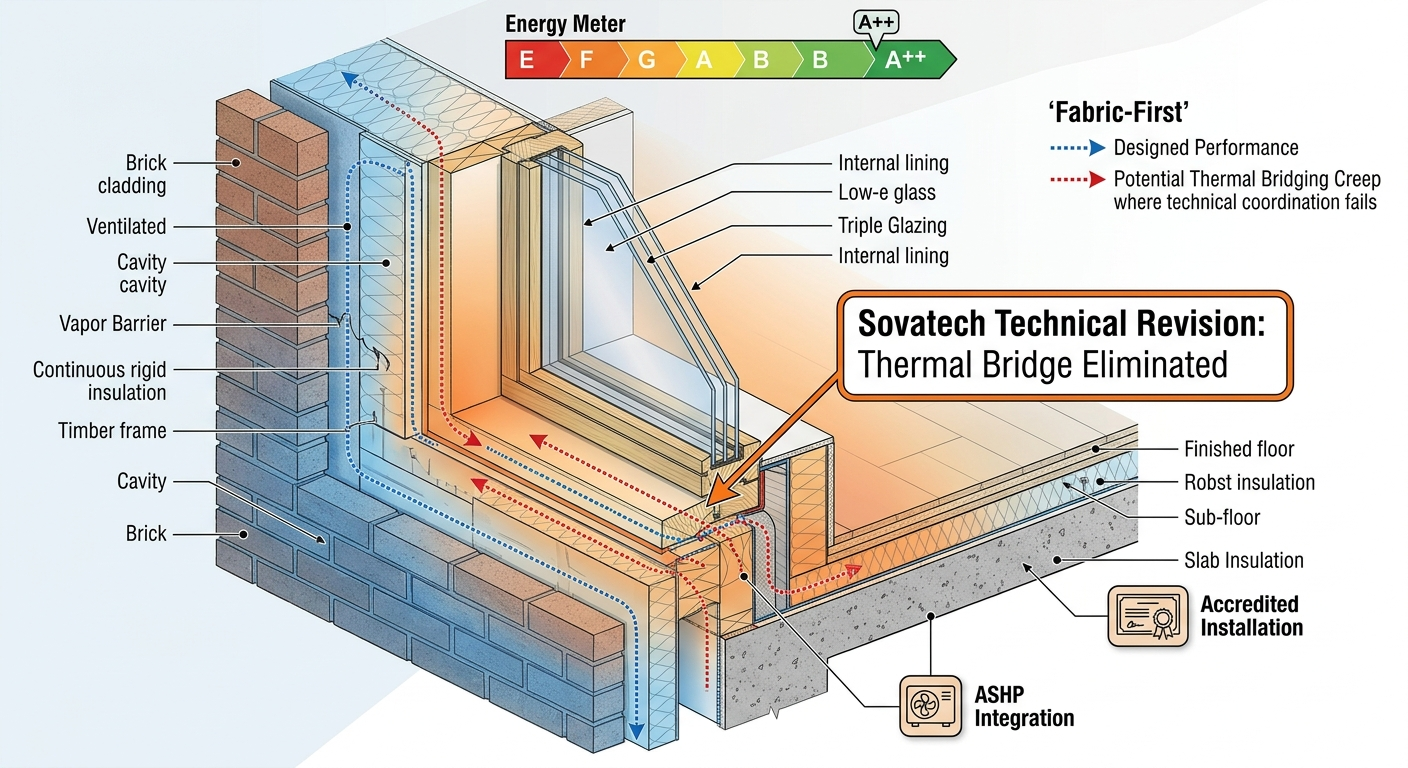

We've moved past the era where you could add a few panels to meet Part L. The Warm Homes Standard demands a holistic approach to the building envelope — air-source heat pumps as the default, high-performance glazing becoming the norm, thermal bridging details that require precision in both design and site execution, and airtightness standards that make MVHR not just desirable but necessary for indoor air quality.

The Warm Homes Plan estimates that a typical household installing a heat pump, solar PV, and battery storage could save up to £550 per year on energy bills (DESNZ analysis). That's a powerful sales message — but only if the systems are designed and installed to perform as intended. And that brings us to one of the most significant risks for developers: the performance gap.

The Performance Gap Risk

If the technical design doesn't match the site execution, the energy performance won't hit the targets — and the regulatory and reputational consequences follow. A heat pump sized for a building with an airtightness of 3 m³/h/m² won't deliver its rated efficiency if the as-built airtightness is 5 m³/h/m² because of poor detailing around service penetrations or window reveals.

This isn't a theoretical concern. The performance gap between designed and as-built energy performance has been well documented across the industry for years. The difference under the FHS is that the gap becomes more consequential — because the systems are more interdependent and the margins are tighter. A poorly commissioned MVHR system doesn't just waste energy; it creates condensation, mould, and customer complaints. A heat pump installed without adequate consideration of emitter sizing, flow temperatures, and hot water cylinder capacity will underperform and generate higher-than-expected running costs.

For developers, managing this gap requires technical precision from design through to handover — ensuring that construction drawings accurately reflect the energy strategy, that site teams understand the critical tolerances, and that commissioning is treated as a technical process rather than an administrative formality.

Heat Pumps Are the Primary Technology — Hydrogen Effectively Ruled Out

The Warm Homes Plan states that hydrogen is "not yet a proven technology for home heating" and that any future role would "come later and likely be limited." Biomethane gets a slightly warmer reception — the government intends to consult on whether it could play a role for properties with few other options to decarbonise — but for new-build residential development, the message is unequivocal: heat pumps are the answer.

The government has set an ambition of 450,000 heat pump installations per year by 2030, up from around 180,000 currently. It wants 70% of UK-installed heat pumps to be manufactured domestically by 2035 — a significant supply chain signal. The Boiler Upgrade Scheme grant has been maintained at £7,500 per installation and extended to cover air-to-air heat pumps for the first time.

For developers, the supply chain question is becoming critical. Heat pump manufacturers are scaling up, but demand is about to accelerate significantly as the FHS takes effect. Developers who establish supply chain relationships now — testing products, training installation teams, building experience with commissioning and handover — will be in a stronger position than those who wait until the deadline forces their hand.

The Electricity-to-Gas Price Ratio — The Unresolved Challenge

This is the one area where the Warm Homes Plan falls short from a developer perspective. The electricity-to-gas price ratio currently sits at around 4.1 — meaning electricity costs roughly four times as much as gas per unit of energy. This ratio is critical because it directly affects whether heat pumps are demonstrably cheaper to run than gas boilers.

A well-installed heat pump with a seasonal coefficient of performance (SCOP) of 2.8–3.0 can offset the price differential through efficiency gains — extracting 2.8–3.0 units of heat for every unit of electricity consumed. But for customers comparing their current gas bills to projected heat pump running costs, the headline electricity price creates hesitation. And in a sales environment, hesitation kills decisions.

Nesta's analysis of the Warm Homes Plan highlights that without further action to reduce electricity prices relative to gas — for example, by shifting policy costs from electricity bills to gas bills or general taxation — heat pump running costs will remain close to, but not dramatically cheaper than, gas boilers from April 2026.

For developers, this has practical sales implications. The industry will need to educate buyers about total cost of ownership — including solar self-generation that reduces grid electricity consumption, battery storage that captures excess solar for evening use, and smart time-of-use tariffs that reward flexibility. Schemes designed with integrated energy packages will demonstrate the strongest bill savings and the most compelling customer proposition. The narrative needs to shift from "heat pump vs gas boiler" to "energy-independent home vs fossil-fuel-dependent home."

District Heating Enters the Mainstream

The Warm Homes Plan sets a target for heat networks to meet 7% of heat demand by 2035, rising to approximately 20% by 2050. Heat network zoning is set to become law in 2026, with Ofgem taking on the role of heat network regulator — establishing rules on pricing, service resilience, outage management, and consumer protection.

For developers working on higher-density urban schemes, this is increasingly relevant. Local authorities may require new developments within designated heat zones to connect to district heating networks rather than installing individual heat pump systems. This has implications for design, for the commercial terms of energy supply agreements, and for the long-term service charges that affect buyer appetite.

For lower-density suburban and semi-rural development — which is where most SME developers operate — individual heat pumps remain the expected solution. But developers should be aware of local heat mapping exercises and zoning designations, particularly where sites fall within or adjacent to urban areas where heat networks are being planned.

The Iran Energy Crisis: Why This All Matters More Now

The timing of the Warm Homes Plan — and the subsequent acceleration of clean energy policy following the Iran crisis in March 2026 — is not coincidental.

The Middle East conflict has sent global oil and gas prices soaring. Energy Secretary Ed Miliband has responded by bringing forward the next renewables auction, introducing plug-in solar for the first time in Britain, and speeding up the Warm Homes delivery programme. Octopus Energy, the UK's largest energy supplier, reported that solar enquiries jumped 27% in the week the conflict started. The Climate Change Committee has confirmed that the cost of achieving Net Zero is less than the cost of the 2022 Ukraine oil price shock — effectively demonstrating that clean energy investment is cheaper than fossil fuel dependence.

For the housebuilding industry, this creates a powerful tailwind behind the Future Homes Standard. Any developer hoping the FHS might be delayed or watered down should recalibrate that assumption. The government has doubled down — and the consumer mood is shifting with it.

Energy independence — the ability to generate your own electricity through solar, store it in a battery, and heat your home without exposure to volatile fossil fuel markets — is becoming a genuine, tangible selling point for new homes. In 2026, lower running costs are the new "granite countertops." The Warm Homes Plan positions new-build properties as energy-secure assets. Developers who lean into this narrative, rather than treating FHS compliance as a regulatory cost to be minimised, will differentiate their product in an increasingly energy-conscious market.

Practical Implications for SME Developers

Supply Chain Readiness

The Warm Homes Plan forecasts 180,000 new jobs in the clean energy sector and major investment in UK manufacturing capacity. But supply chains don't scale overnight. Heat pump availability, qualified installer and commissioning capacity, MVHR specialist installers, and solar PV supply are all potential bottlenecks as demand accelerates through 2026 and 2027.

Developers should be establishing relationships with heat pump suppliers, solar installers, and MVHR providers now. Running dual specifications — current Building Regulations alongside FHS-compliant designs — on schemes currently in pre-application or detailed design allows you to test supply chains, build installation experience, and identify practical challenges before the deadline.

Design Integration From the Start

The Warm Homes Plan reinforces that solar, heat pumps, batteries, and ventilation work best as integrated systems. This has design implications from RIBA Stage 2 onwards: roof orientation and pitch for optimal solar generation, plant room space for heat pump units and hot water cylinders, electrical infrastructure for battery storage and EV charging, ductwork routes for MVHR systems, and acoustic considerations for external heat pump units.

The challenge for SME developers isn't just the technology — it's the coordination. Ensuring that your architect, M&E engineer, SAP assessor, and energy consultant are working from the same brief, with the same performance targets, and that the resulting technical drawings reflect the integrated energy strategy rather than a collection of disconnected specifications. This is where the "performance gap" is born — not on site, but in the design coordination that precedes it.

For schemes already in detailed design, retrofitting these requirements is expensive and disruptive. For schemes at pre-application or outline stage, there's still time to design them in from the outset — which is always cheaper and produces better outcomes.

Sales and Marketing

The energy crisis has created a consumer environment where energy-efficient homes are valued as a practical financial benefit, not just an abstract environmental aspiration. The Warm Homes Plan's messaging around £550 per year in potential energy bill savings gives developers a credible, government-backed figure to reference in marketing materials — provided the systems are designed and installed to deliver those savings in practice.

Schemes that can demonstrate energy independence — solar generation, battery storage, heat pump efficiency, and smart tariff compatibility — will command a premium in a market where energy costs are front-page news. The developers who treat this as a product feature rather than a compliance burden will win the sales conversation.

The Sovatech Perspective

The convergence of the Future Homes Standard, the Warm Homes Plan, and the Iran energy crisis creates a complex technical landscape for developers to navigate. New specifications, new technologies, new supply chains, and new customer expectations — all arriving simultaneously.

At Sovatech Consulting, we help developers make sense of this complexity. From understanding how FHS requirements affect your technical submissions, to coordinating the consultant inputs needed for compliant planning applications, to ensuring your drawings reflect the design requirements of integrated heat pump, solar, and ventilation systems — we provide the strategic technical input that keeps your projects on track.

We don't just want your homes to be warm and compliant. We want your projects to stay out of the "technical debt" zone — where design assumptions that weren't properly coordinated at the outset become expensive site problems that erode margin and programme.

The regulatory environment is changing faster than at any point in recent memory. Developers who engage technical expertise early — understanding the implications before they commit to designs and land purchases — will protect their viability. Those who wait will find themselves redesigning, re-specifying, and re-costing in a market that has already moved on.

If you're designing schemes that will be built under the Future Homes Standard and need technical support to navigate the regulatory requirements — from pre-acquisition energy feasibility through to planning submissions and compliance coordination — contact Sovatech Consulting. We'll help you understand what's changing, what it means for your projects, and how to prepare.